The IRS does not negotiate with fear. It collects from it. When you’re carrying significant tax debt and watching penalties compound month after month, the gap between what you owe and what you could actually settle for is not obvious — and most people never find out because they wait too long, hire the wrong help, or assume the number on the notice is the final word.

Tax resolution ROI is the measurable difference between what a taxpayer owes the IRS before professional intervention and what they actually pay to resolve that debt — including penalties, interest, and fees — expressed as a percentage of the original balance.

Key Takeaways

- Certified tax resolution specialists routinely negotiate settlements at 5–15% of the original balance owed, though outcomes depend heavily on financial disclosure and case timing.

- The IRS has specific relief programs — Offer in Compromise, Currently Not Collectible status, Penalty Abatement — that most general tax preparers never use because they don’t specialize in collections work.

- Weak results almost always trace back to one root cause: the taxpayer or their representative failed to build a complete financial picture before approaching the IRS.

- BPB Tax Resolutions has eliminated over $1.2 million in client debt, with average client savings of 50% of the original tax balance.

- Every day without a resolution strategy is a day penalties and interest accrue — the IRS does not pause while you decide.

What Does Strong IRS Tax Resolution ROI Actually Look Like?

Strong results are specific. Not “we helped you feel better about your taxes” — actual dollar amounts, documented settlements, and enforcement actions stopped.

Here is what a strong outcome looks like in practice:

- Wage garnishment halted within 24–72 hours of a specialist invoking IRS representation rights under Form 2848 (Power of Attorney). The mechanism: once the IRS receives that form, by law it must direct all communication to the representative — not the taxpayer. The garnishment doesn’t stop because someone asked nicely. It stops because the IRS is legally required to pause enforcement while the case is under active review.

- Settlement at 5–15% of original balance through an accepted Offer in Compromise (OIC). The IRS’s own data, published annually in the IRS Data Book, shows acceptance rates for OICs hover around 40% in recent years — meaning roughly four in ten submitted offers get accepted. The difference between accepted and rejected almost always comes down to how the financial disclosure package was constructed.

- Penalty abatement that eliminates 20–40% of the total balance before any settlement negotiation even begins. Most taxpayers don’t know this exists. First-time penalty abatement is an administrative waiver the IRS grants to taxpayers with a clean prior compliance history — it requires no special circumstances, just proper application.

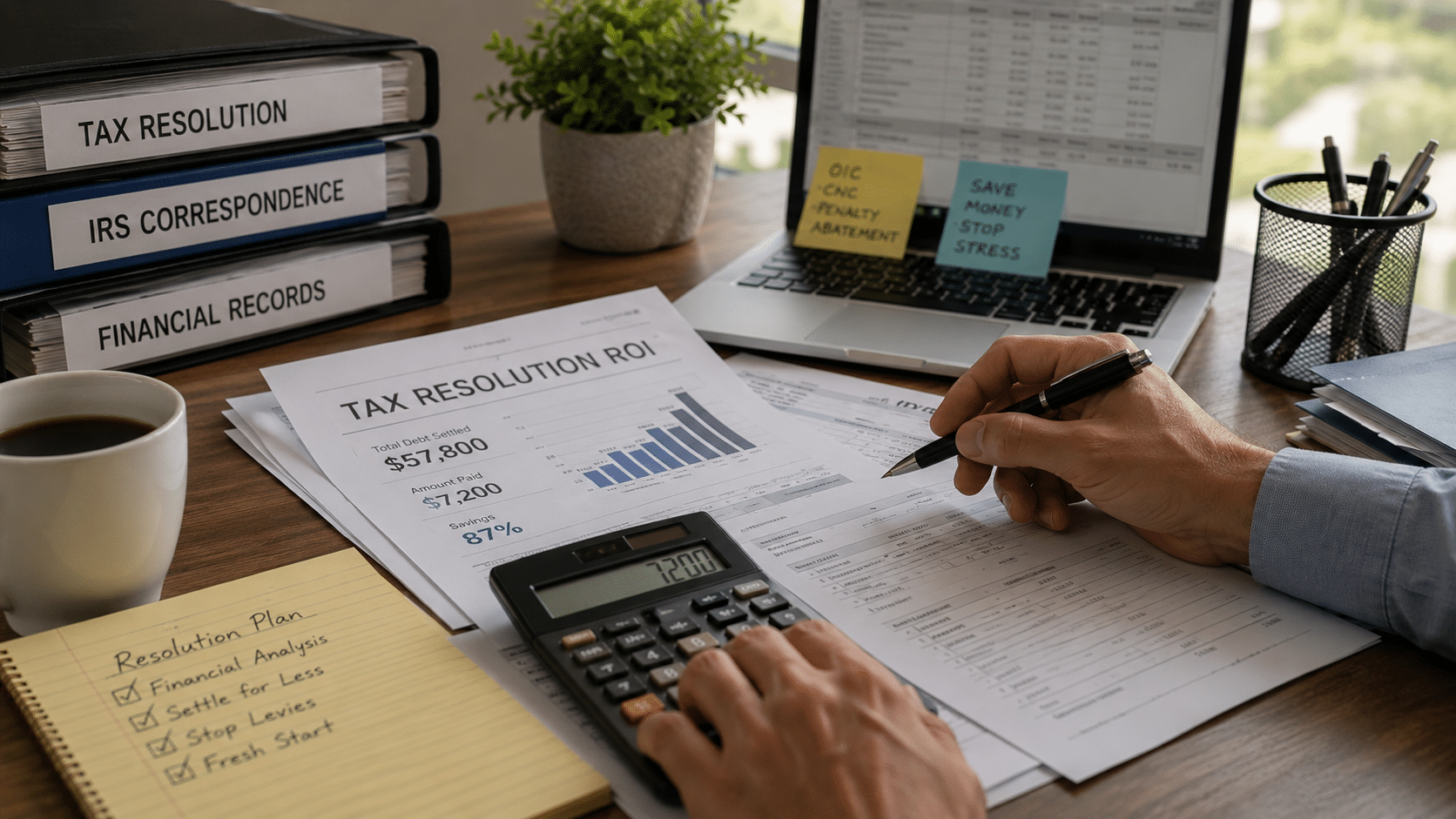

A real case pattern: A self-employed contractor three years into penalty accrual on a $68,000 balance engaged BPB Tax Resolutions. After penalty abatement reduced the balance to approximately $51,000, an Offer in Compromise was submitted and accepted at $7,200 — roughly 11% of the original amount owed. Total resolution timeline: 14 months from first contact to final IRS acceptance letter.

That is what strong looks like. Numbers, mechanism, timeline.

What Does Weak ROI Look Like — and Why Does It Happen?

Weak results are not random. They follow a pattern.

The most common failure mode: a taxpayer hires a general CPA or tax preparer who files back returns competently but has no specialized training in IRS collections negotiation. The returns get filed. The balance gets confirmed. No one pursues abatement, no one submits an OIC, no one requests Currently Not Collectible status. The taxpayer ends up on an Installment Agreement paying the full balance — plus interest — over years.

The contrarian claim: paying the IRS back in full is often the worst financial outcome, not the safest one. Most people assume that settling for less than owed is risky or aggressive. The opposite is true. The IRS created the Offer in Compromise program specifically because collecting a fraction of an uncollectible debt is better than collecting nothing. Pursuing full payment from someone who qualifies for settlement is leaving money on the table — yours, not theirs.

The second failure pattern: waiting. Practitioners consistently observe that cases initiated within the first 12 months of IRS collection activity resolve faster and at lower settlement amounts than cases where the taxpayer waited 3–5 years. Why? Because penalty and interest accrual is exponential, not linear. A $30,000 balance ignored for four years can easily become $55,000 before a single negotiation begins.

The IRS does not get emotional about collections. It just keeps moving.

The Resolution Readiness Framework: What Separates Settled Cases From Stalled Ones

Resolution Readiness is the degree to which a taxpayer’s financial disclosure is complete, accurate, and strategically presented before any IRS negotiation begins.

BPB Tax Resolutions uses what practitioners in this field call a pre-negotiation financial architecture — building the complete picture of income, expenses, assets, and liabilities before making any offer or request to the IRS. This is not paperwork. This is strategy.

The IRS evaluates OIC eligibility using a formula based on Reasonable Collection Potential (RCP) — the IRS’s own term for what they believe they can realistically collect from you. If your RCP is lower than what you owe, you may qualify for a settlement. The entire job of a skilled specialist is to document your RCP accurately and completely.

Use this framework when:

You have documented income below IRS collection thresholds

You have significant allowable expenses (medical, housing, transportation) that reduce disposable income

You have limited equity in assets the IRS could seize

Do not attempt an OIC without professional help when:

Your financial picture is incomplete or inconsistent

You have unfiled returns (the IRS will reject an OIC if you’re not in compliance)

You have significant liquid assets that exceed the settlement amount you’re targeting

The single most important insight in this entire article: the IRS does not settle based on what you owe — it settles based on what it believes it can collect. Those are two completely different numbers.

How Does BPB Tax Resolutions Compare to Other Options?

| Option | Typical Outcome | Timeline | Cost | Risk |

| Do nothing | Escalating garnishments, liens, levies | Immediate enforcement | Highest — full balance plus penalties | Severe |

| General CPA / tax preparer | Back returns filed; full balance confirmed | 3–6 months | Moderate fees | Moderate — no settlement negotiation |

| Tax attorney | Legal representation; strong for litigation | 6–18 months | High hourly fees | Low legal risk; high cost |

| IRS payment plan (self-negotiated) | Full balance paid over time with interest | Ongoing | No professional fees | Moderate — no reduction in balance |

| Certified Tax Resolution Specialist (BPB) | Settlement at 5–15% of balance; garnishments stopped; liens removed | 30 days to 18 months depending on complexity | Flat fee structure; free 15-min assessment | Low — specialists know exactly which programs apply |

The tradeoff worth naming honestly: tax resolution specialists are not the right fit for simple tax situations. If you owe under $10,000 and have a straightforward income picture, an IRS payment plan may be entirely sufficient. BPB Tax Resolutions is built for complex, high-balance situations where the gap between what you owe and what you could settle for is large enough to justify professional negotiation.

Who Is This NOT For?

Not every tax situation needs a resolution specialist. This approach does not apply when:

- Your balance is under $10,000. The IRS has streamlined installment agreements for smaller balances that require minimal negotiation.

- You are looking for a way to avoid legitimate tax obligations entirely. Tax resolution is legal negotiation within IRS-defined programs. It is not tax evasion strategy.

Honest framing matters here. A firm that tells every prospect they qualify for a 90% reduction is not being straight with you.

7 Questions People Actually Ask About IRS Tax Resolution ROI

How long does it actually take to settle IRS debt? Most cases with BPB Tax Resolutions resolve in 6 to 18 months, depending on complexity and whether back returns need to be filed first. Wage garnishments can be stopped within 24 to 72 hours of representation, but full settlement through an Offer in Compromise typically takes 12 to 18 months from submission to IRS acceptance.

Can the IRS really come after my wages and bank account at the same time? Yes. The IRS can issue simultaneous wage garnishments and bank levies once a taxpayer is in active collections status. A certified tax resolution specialist can invoke representation rights under IRS Form 2848, which legally requires the IRS to halt direct contact and enforcement actions while the case is under active review.

What happens if the IRS rejects my Offer in Compromise? A rejected OIC does not close your options. You can appeal the rejection, resubmit with a stronger financial disclosure package, or pursue alternative relief programs like Currently Not Collectible status or a formal Installment Agreement. BPB Tax Resolutions evaluates which path makes sense based on the specific reason for rejection.

Does hiring a tax resolution specialist trigger an audit? No. Engaging professional representation does not increase audit risk. In fact, having a certified specialist manage IRS communication reduces the likelihood of inadvertent disclosures that could complicate your case — a common risk when taxpayers communicate directly with IRS agents without preparation.

What is Currently Not Collectible status and how does it help me? Currently Not Collectible (CNC) status is an IRS designation that temporarily halts all collection activity — garnishments, levies, and liens — when a taxpayer’s income does not exceed their allowable living expenses. It is not a permanent resolution, but it stops the immediate bleeding while a longer-term strategy is developed. BPB Tax Resolutions uses CNC status strategically as a bridge in complex cases.

What does a tax resolution specialist actually do that I can’t do myself? The core value is not paperwork — it is knowing which IRS programs apply to your specific financial situation and how to present your case to maximize your Reasonable Collection Potential calculation in your favor. The IRS processes millions of cases; a specialist knows exactly how to structure a submission so it doesn’t get rejected on procedural grounds before it’s ever reviewed on merit.

How do I know if BPB Tax Resolutions is the right fit before I pay anything? BPB Tax Resolutions offers a free 15-minute Tax Health Assessment with no high-pressure sales approach. In that conversation, Ben Butterfield’s team will tell you honestly whether you qualify for settlement programs and what a realistic outcome looks like for your specific situation — before you commit to anything.

If you’ve read this far, you already know your situation is serious enough to warrant a real answer — not a general explanation of IRS programs, but a specific assessment of what your number could actually be.

Call BPB Tax Resolutions today and ask for your free Tax Health Assessment. Not because it costs nothing — because in 15 minutes, you will know exactly what you’re dealing with and whether there is a real path to settling your debt for a fraction of what the IRS says you owe. That clarity is worth more than another week of unopened IRS notices. If you want to understand the assumptions that quietly inflate what most taxpayers end up paying, that context matters before you make any decisions.

Visit bpbtaxresolutions.com or call to schedule your assessment now.

References

IRS — IRS Data Book (published annually), covering Offer in Compromise acceptance rates, collection statistics, and enforcement activity across fiscal years.

IRS — Form 2848, Power of Attorney and Declaration of Representative, governing taxpayer representation rights before the IRS.

IRS — Internal Revenue Manual, sections covering Offer in Compromise eligibility, Reasonable Collection Potential calculations, and Currently Not Collectible status criteria.

IRS — First-Time Penalty Abatement administrative waiver policy, available at IRS.gov under penalty relief information.